With the rise of point of sale (POS) lending, the method through which fintech platforms get approvals for their consumers is often overlooked. When a consumer fills out an application, the process a fintech uses to get that application checked against the lenders they work with affects the speed of the approval, the quality of the offer, and the variety of options displayed.

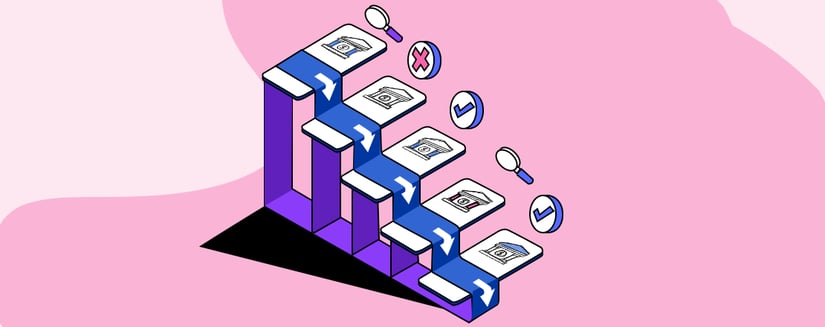

One of the most popular processes utilized by fintech platforms is called waterfall lending. This process checks applications against lender criteria one lender at a time to ensure that a consumer gets the best possible approval.

However, it has its benefits and drawbacks, so we are going to break down the following:

- What waterfall lending is

- The pros and cons of waterfall lending

- The alternative process used by other fintechs

What Is Waterfall Lending

Waterfall lending is the process of checking consumer applications against lenders one at a time, from the most prime lender to the least. If the best lender doesn’t provide an approval, the application is sent to the next best option, and so on, until an approval is given or the application is declined entirely.

This process ensures that each application gets multiple chances for an approval before a client is ever declined, and it rewards better lenders that offer more advantageous terms for consumers. If multiple approvals are given for the same application, consumers can choose from the different terms on many platforms, giving them the flexibility to select a deal that works for them.

The Pros and Cons of Waterfall Lending

As we mentioned above, there are benefits and drawbacks to this approach.

The benefits of waterfall lending are that applications are reviewed under a wide variety of criteria. This increases the odds for approval, meaning they are more likely to be able to finance their purchase and less likely to be turned away from a purchase altogether by a declination. This makes it attractive to merchants since it reduces the risk of losing customers by offering POS financing.

The drawbacks of waterfall lending are that it can take more time than other processes used for POS financing, like simultaneous lender matching, since it checks the application against different lenders one at a time. Since it is all automatic, it can still be fast but struggles to be near-instant if the fintech platform works with a large number of lenders. This disincentivizes the financing platform from adding more lenders to its network, as it risks making the approval process slower. It also adds more friction to the purchase process for consumers.

To make this a little more clear, the chart below sums up the pros and cons of waterfall lending.

Pros✔ Wide variety of funding sources. ✔ Higher approval odds for consumers than a single lender approach. ✔ Rewards lenders that offer better terms ✔ Ensures that more customers get financing offers. ✔ Streamlines the process by using one application for the customer. ✔ Theoretically allows for as many lenders as needed. |

Cons✘ Slower than other methods (like simultaneous lender matching). ✘ Disincentivizes adding more lender variety. ✘ Creates friction in the purchase process. ✘ Some lenders do hard pulls, which can create repeated inquiries on the customer's credit profile. ✘ Each lender has to deny the application before it moves to the next lender, which can create time delays for the customer. ✘ Customer data is being sent from lender to lender. ✘ The lender flow only goes one direction and is not customizable. ✘ Limited opportunity to incorporate niche lenders when needed only for a few SKUs. |

The Alternative Process: Simultaneous Lender Matching

The other option used by fintech platforms to gather approvals from a wide network of lenders is simultaneous lender matching. This involves checking an application against multiple lenders, just as waterfall lending does, but doing so with all possible funding sources simultaneously. This speeds up the process by not waiting for each individual check to be complete. This allows the platform to involve as many lenders as possible, and it won’t slow down the approval process.

This also adds more variety for the consumer, as the process doesn’t end once a single funding source has given an approval. This allows the platform to display and prioritize every approval that the consumer received, maximizing their freedom of choice.

This is the process used by Skeps.

Beat Waterfall Lending With Skeps

Skeps offers a comprehensive, end-to-end consumer financing platform that helps lenders and merchants connect with convenient and modern financing options. Working with an entire network of established lenders and a wide variety of merchant partners, we go above and beyond instant installment payment plans. We help lenders offer a few different types of consumer financing through third-party merchants, including:

- Instant installment financing

- Co-branded credit cards

- Consumer loans and leases

If you’re looking to partner with a forward-thinking fintech company that will get your financial products in front of as many consumers as possible, Skeps is the perfect fit.

Do you have more questions about the pros and cons of waterfall lending vs. simultaneous lender matching? Request a demo today or email us at support@skeps.com.